.png?width=50&name=headshot-vp%20(2).png)

Since the Strait of Hormuz closure on February 28, JKM and TTF have been competing for every...

20% of global LNG supply is now offline. QatarEnergy halted production at Ras Laffan this morning after Iranian drones struck the facility as part of Tehran's retaliation for US-Israeli strikes on Iran leading to effective closure of the Strait of Hormuz over the weekend. US LNG feedgas peaked above 19 Bcf/d in December and is currently running near 18.8 Bcf/d, effectively at capacity. There may be no immediate spare capacity to backfill this. And for the first time since 2022, the market has to price that reality with EU storage at multi-year lows and injection season weeks away.

The Halt

Following coordinated US-Israeli strikes on Iran, Tehran launched retaliatory drone and missile strikes across the Gulf, targeting US bases, allied infrastructure, and energy facilities. Qatar's Ministry of Defense confirmed two Iranian drones hit Qatari soil: one struck a water tank at a Mesaieed power plant, the other targeted an energy facility at Ras Laffan Industrial City. No casualties were reported, but QatarEnergy cited the attacks directly in halting all LNG production and associated operations at both sites. The IRGC's effective closure of the Strait of Hormuz compounds the disruption: every molecule of Qatari LNG transits the Strait. So does the UAE's Das Island output (~6 MTPA (~0.8 Bcf/d) from ADNOC). Combined, the disruption removes roughly 20% of global LNG supply, over 80 MTPA (~10.5 Bcf/d), from the market in real time. QatarEnergy, the world's largest LNG supplier at 77 MTPA (~10.1 Bcf/d) nameplate capacity, has given no timeline for resuming operations.

TTF surged over 35% around $14/MMBtu. JKM spiked to $15.06/MMBtu (up 39%). UK NBP followed with similar gains.

What Leviaton Shows

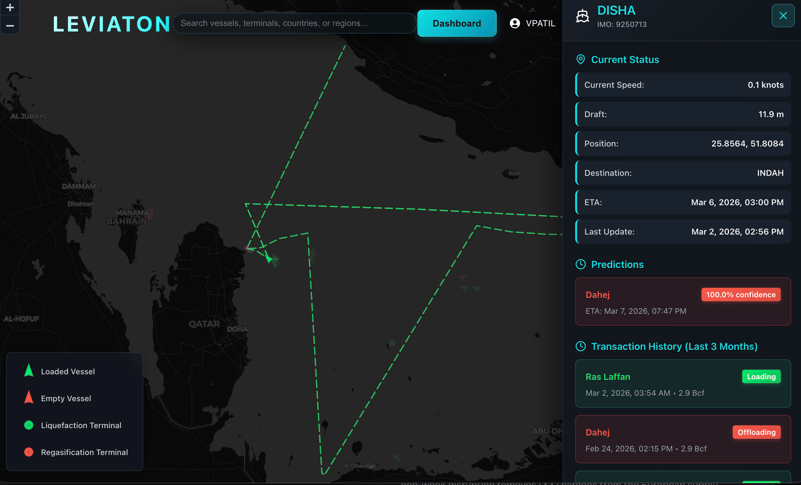

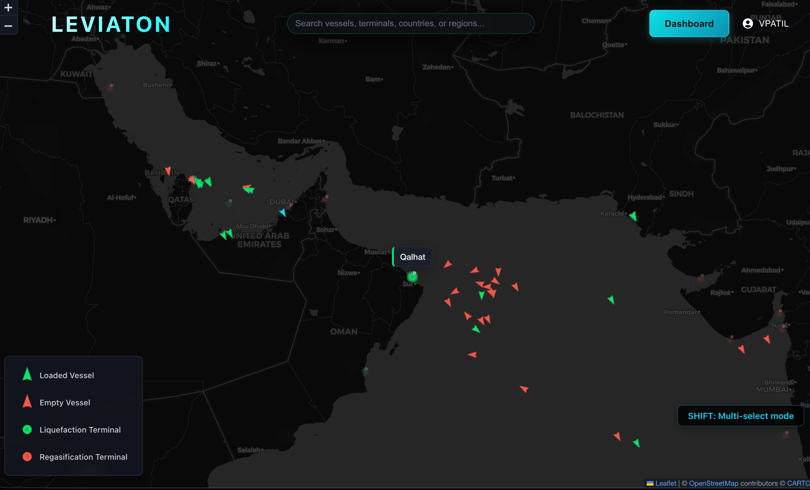

SynMax Leviaton vessel tracking confirms AIS signal manipulation across the Strait, consistent with IRGC electronic interference reported by UKMTO.

Ballast LNG carriers are stacking near Oman in the Arabian Sea, unable to proceed to Ras Laffan for loading.

Europe’s Exposure

European gas storage sits at approximately 29.9% as of writing of this article, the lowest for this time of year since the 2022 energy crisis. Europe entered winter 2025/26 already behind, with storage at just 61% at year-end versus 72% the prior year. A prolonged halt does not hit immediately, average sailing time from Ras Laffan to Northwest Europe via the Cape of Good Hope is ~34 - 40 days, but the refill math is brutal. Even a one-week disruption removes 2-3 (8-9 bcf) cargoes from the European supply at a time when injection season is weeks away.

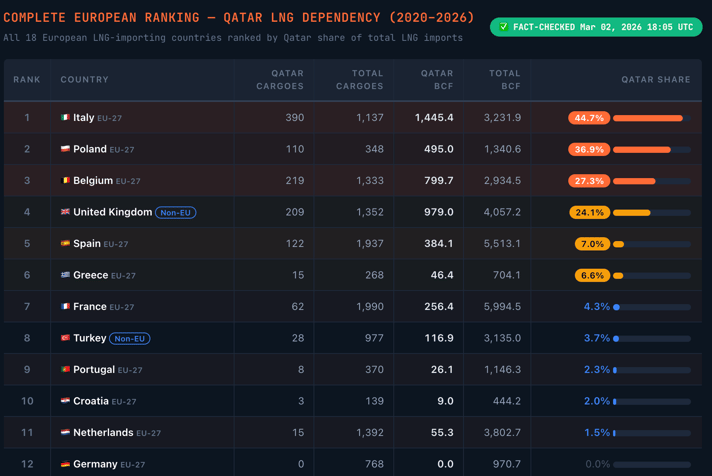

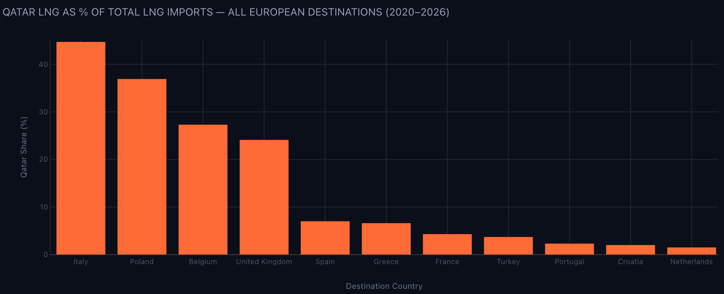

Italy, Belgium, and Poland remain the most exposed to Qatari LNG volumes among EU importers via existing long-term contracts, collectively absorbing nearly 78% of all Qatari LNG delivered to the EU-27 since 2020. Outside the EU, the UK, Europe's fourth-largest Qatari LNG recipient, sources 24% of its total LNG imports from Qatar, making it the most exposed non-EU buyer on the continent.

If those flows go to zero for any sustained period, Mediterranean and Northwest European regas terminals face a shortfall that US and West African cargoes would struggle to backfill at current capacity. The pricing pressure on spot TTF cargoes redirecting from these routes will be felt immediately across the entire European gas curve.

Asia Is Competing for the Same Molecules

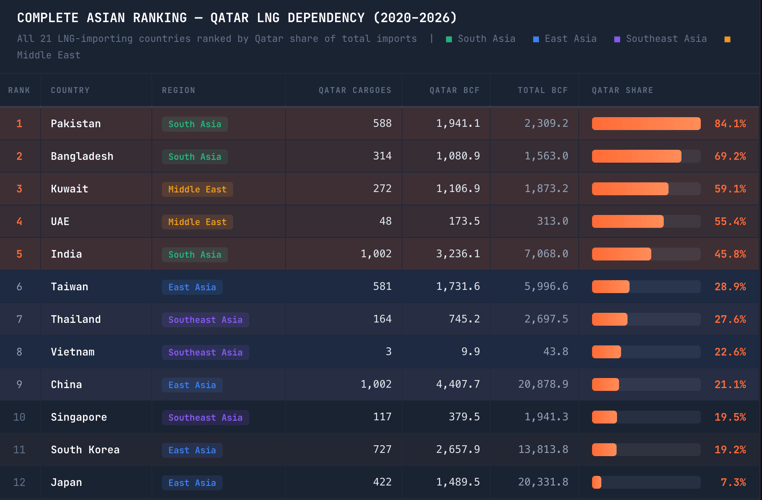

Asia's exposure to Qatari LNG dwarfs Europe's by every measure. Since 2020, Asia has absorbed four times more Qatari LNG than the entire European continent. Five Asian nations source over 40% of their LNG from Qatar: Pakistan (84%), Bangladesh (69%), Kuwait (59%), the UAE (55%), and India (46%), countries with limited alternative supply and, in several cases, no meaningful domestic gas production to fall back on. China alone receives nearly as much Qatari LNG as all of Europe combined. South Korea sources 19% of its LNG from Qatar, Taiwan 29% .

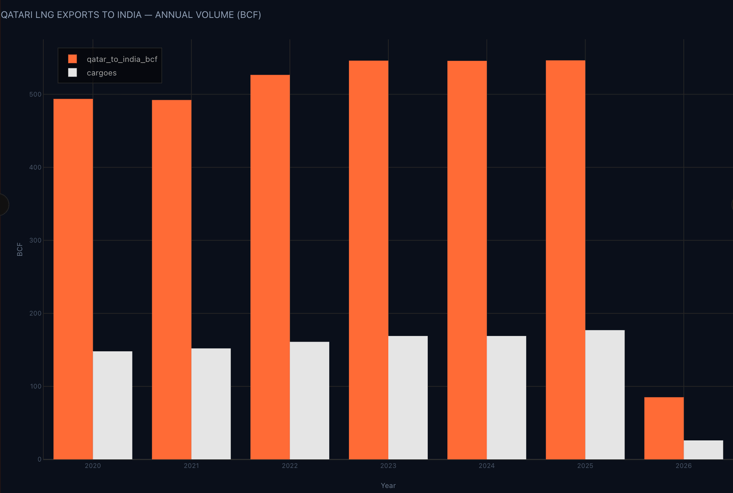

India's exposure is particularly acute. The country is one of the world's largest LNG importers, taking in over 1,201.7 bcf in 2025, of which 546.5 bcf came from Qatar. Petronet LNG's 7.5 MTPA (1 Bcf/d) contract with QatarEnergy, renewed in early 2024 as a $78 billion, 20-year deal running through 2048, alone accounts for roughly 35% of India's total LNG imports. With the government targeting more than a doubling of gas in the energy mix by 2030 and domestic production in structural decline, India's LNG import needs are set to more than double this decade. Nearly all of that growth was expected to flow through Qatar's expansion.

In total, nine Asian countries depend on Qatar for more than a fifth of their LNG supply. If the Strait of Hormuz remains closed for any sustained period, the supply shock to Asia will be multiples of what Europe faces, and unlike Europe, which spent three years diversifying away from Russian pipeline gas, Asia has had no comparable wake-up call to reduce its Qatar dependency.

Following the developments, Japan, South Korea, China, and Taiwan are all now competing for every non-Hormuz LNG cargo out there available. South Korea's Ministry of Trade convened an emergency energy meeting today to evaluate supply chain exposure. Taiwan announced a 3% increase in consumer gas prices even before the Strait closed, reflecting LNG cost pressures that predated this crisis. Greek-flagged tanker owners, who control a significant share of global LNG carrier capacity, have been instructed to avoid the Persian Gulf, the Gulf of Oman, and the Strait entirely.

The dynamic is straightforward: with Qatar offline, Asian buyers who relied on Ras Laffan cargoes will redirect to spot markets, bidding against European utilities for every available US Gulf Coast, West African, and Australian cargo. That demand-side competition is what makes the US capacity ceiling so brutal. It is not just Europe pulling harder on American molecules. It is every major LNG importing region pulling harder on the same 18.8 Bcf/d.

US LNG Is the Only Game Left, and It's Maxed Out As of Now

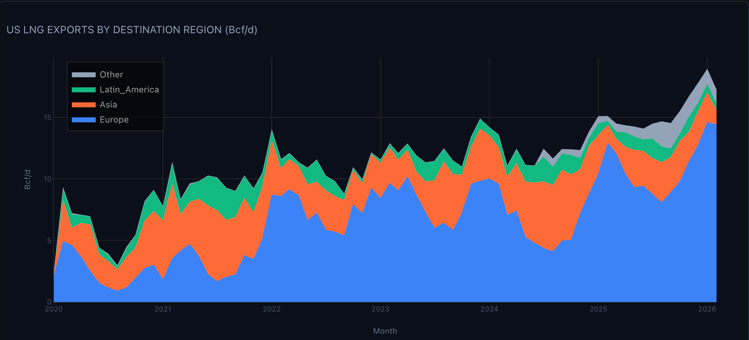

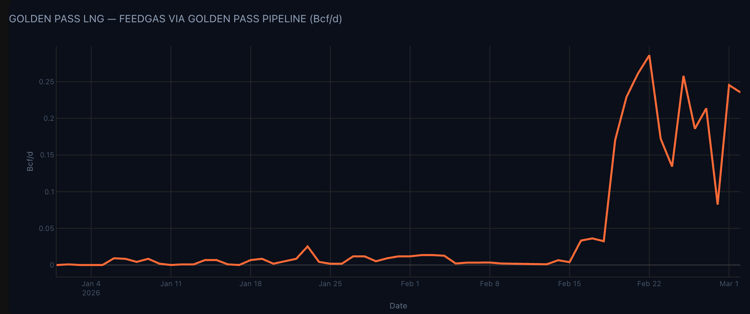

US LNG feedgas averaged over 19 Bcf/d in December. Exports hit 18.4 Bcf/d, a record. Every operational terminal was at or above nameplate. You cannot push more through existing infrastructure, the constraint is physical, not commercial. The US accounted for 58% of Europe's LNG imports in 2025. Corpus Christi Stage III is still ramping up, but incremental gains from commissioning trains do not replace 77 MTPA (~10.1 Bcf/d) of Qatari supply. Some near-term relief is Golden Pass LNG Plant.

Golden Pass Train 1 is ramping up. With Ras Laffan offline and QatarEnergy controlling 70% of the facility, Train 2 and Train 3 development timelines may need to be fast-tracked to meet the supply gap. Whether that is operationally realistic during an active conflict involving the majority owner is the open question.

The contract market reinforces the thesis. Today, Venture Global and Trafigura signed a 5-year binding SPA for 0.5 MTPA (~0.07 Bcf/d) commencing 2026. Last week, Venture Global signed a 20-year SPA with Hanwha Aerospace for 1.5 MTPA (~0.20 Bcf/d). The Trafigura deal signals how trading houses are positioning: mid-term, portfolio optionality as the premium in a market where spot is repricing violently.

The TTF-to-Henry Hub spread is widening at exactly the moment there is no incremental capacity to capture it. Europe's refill season begins in April. The longer Ras Laffan stays offline, the stronger the case for locking in long-term US LNG contracts.

Source: SynMax Intelligence. Leviaton vessel tracking and LNG flow data. Hyperion natural gas production and feedgas monitoring. Analysis generated with support from SynMax Agents. Data as of March 2, 2026.

Dashboard link: https://hyperionagents.synmax.com/public/dashboard/1493f3dadeda1e8ff7e8d9876a0f667b2f91b0917a5117fa877eae13a70f24c1