There are important differences between the assumptions in our short and long term forecasts, which have been highlighted in recent months. Ideally, we want these two forecasts to tell similar stories, to do that there are two major factors that need to be added to the STF.

-

Shut-ins: We currently believe there are 0.80 bcfd of wells shut in in SW PA. We are accounting for this dormant prod coming back online in the LTF but not the STF.

-

DTILs: There is around 1.9 bcfd of delayed TIL wells in the northeast that is not accounted for in our STF but is accounted for in our LTF.

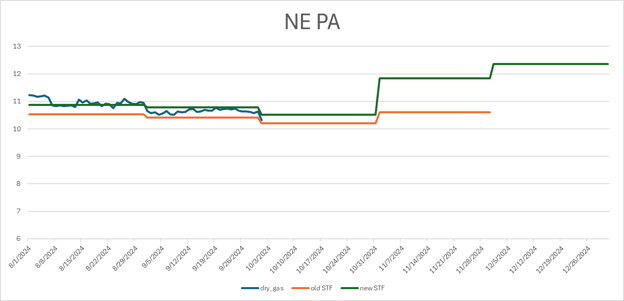

Adding DTILs to the NE PA STF

We have updated our STF for NE PA to include our base case assumption that DTILd wells will turn in line bringing a production increase in November. The revised model is launching today. The effect of bringing these wells into production quickly would cause NE PA prod to increase from an expected 10.5bcf/d in October to 11.84 bcf/d in November. This increase is sudden and while we see this as the most likely scenario given market incentives we believe, although less strongly, that producers may bring these DTILs online more gradually through the winter causing a similar increase in production but more spread out over the season.

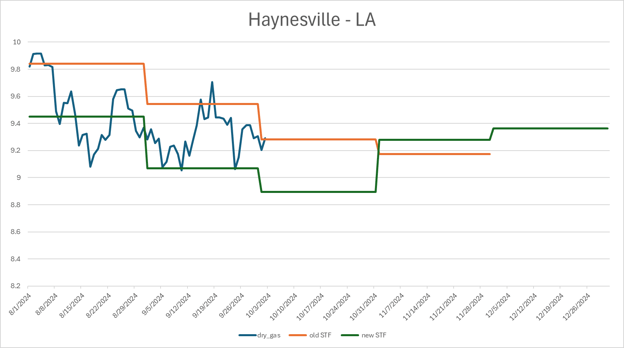

Adding DTILs to the Haynesville - LA STF

In the Haynesville DTILs are much smaller so while adding them does increase forward looking production it does not have the same kind of impact as NE DTILs. Also included in this model update is the latest state production data which has pulled the STF down somewhat. This is better matching our daily production model but it is also offsetting some of the DTIL growth.

Summary

These changes help our STF better align to our LTF but do not fully close the gap. Since the STF is a well level model adding in the return of shut-ins becomes complicated as it needs to be distributed to individual wells. We are working on ways to do that. Furthermore the LTF is constructed using a different methodology, primarily producer production guidances. Our aim is not to make these two forecasts match exactly, rather we want to find consensus in the evolution of production using two completely independent methods. We believe the exercise of modeling forward production from these two perspectives helps us better understand near and long term trends.