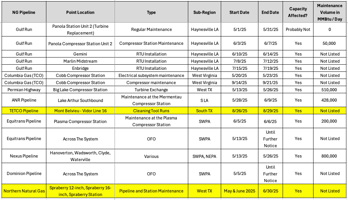

NG Pipeline Point Location Type Sub-Region Start Date End Date Capacity Affected? Maintenance...

Earnings Highlights APA, MTDR, MUR, & SM

APA Corporation (APA)

APA is sustaining flat US oil production at ~122 Mbo/d (raised from prior 120-122 range) on materially lower 2026 capex (Permian $1.3B, -20% YoY; total upstream $2.1B, -10%) by holding rigs flat at 5 and TILs at ~130 (vs 140 in 2025), driven by D&C and cost reductions per lateral foot. US natural gas continues to step down — implied FY26 ~0.435 Bcf/d vs ~0.504 Bcf/d FY25 (-13.7% YoY) reflecting divestments, natural decline, and active curtailments at Waha (88 MMcf/d in Q1 2026, 91 MMcf/d in Q4 2025) with a further ~35 Mboe/d total curtailment expected in 2Q 2026 before assumed normalization in 2H 2026.

Read the full analysis on the dashboard.

Matador Resources (MTDR)

MTDR delivered FY2025 natural gas production of 0.524 Bcf/d (524.1 MMcf/d) and guided FY2026 to 0.525-0.545 Bcf/d (mid 0.535 Bcf/d, +2% YoY) — gas guidance was REAFFIRMED unchanged in the Q1 2026 deck even as oil and total BOE/d guidance were raised.

2025 efficiency wins compounded into 2026: D&C cost per lateral foot fell from $910 (2024) → $842 (2025) → guided $785-805 (2026E mid $795, -6% YoY), driven by ~10% longer laterals, ~13% faster cycle times, 50% batch development, simul- and trimul-frac, 90% diesel reduction in completions, 72% produced-water frac use, and AI integration with vendor partners.

Read the full analysis on the dashboard.

Murphy Oil Corporation (MUR)

Murphy Oil reaffirmed its FY 2026 production guidance of 167–175 MBOEPD (mid 171) in the Q1 2026 deck — unchanged from the Q4 2025 deck — implying a total-company natural gas guide of ~0.45 Bcf/d (range 0.41–0.50), down ~10% YoY from 2025's actual ~0.50 Bcf/d, with U.S. gas (Eagle Ford + Gulf of America) implied at ~0.07 Bcf/d vs ~0.08 Bcf/d in 2025 (–12% YoY). The Q1 2026 deck quantified record-breaking Eagle Ford efficiency.

Read the full analysis on the dashboard.

SM Energy (SM)

SM Energy closed its transformative Civitas Resources merger on January 30, 2026, transforming SM from a single-region (Permian + Uinta) operator into a four-basin scaled producer (Permian, DJ, South Texas, Uinta); on an asset-mix-adjusted basis (normalizing for the Civitas oil-weighted contribution) SM's FY 2026 implied natural gas guidance is approximately 0.42 Bcf/d, versus FY 2025 actual of 0.41 Bcf/d — a YoY increase of approximately +2.5%.

Read the full analysis on the dashboard.

As usual, contact support@synmax.com with questions.